If you’ve ever opened a hospital bill after insurance kicked in, you already know the shock.

A few nights in the hospital can still leave you owing thousands—even with a solid health plan.

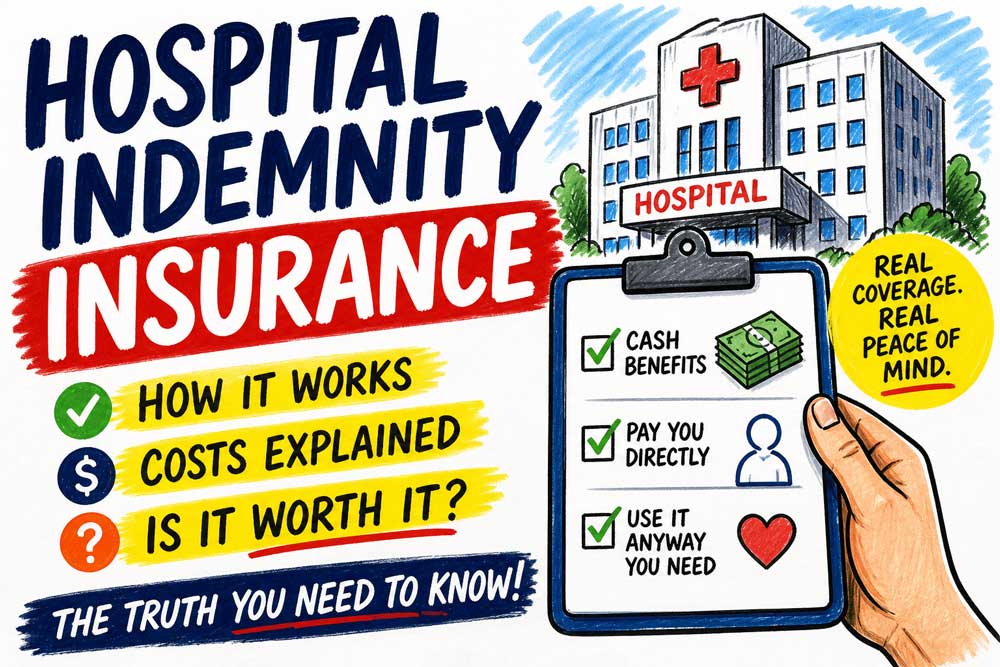

That’s where hospital indemnity insurance comes in.

It’s not flashy, and it’s often misunderstood – but for many Americans, it acts like a financial shock absorber when life takes an unexpected turn.

In this guide, you’ll learn what hospital indemnity insurance is, how it works, and whether it’s actually worth paying especially if you’re planning a pregnancy, managing a high-deductible plan, or protecting your family’s finances.

Quick Precap

- Hospital indemnity insurance pays cash directly to you

- It’s best for high-deductible plans and predictable hospital events

- It’s not a replacement for health insurance

- Costs are relatively low, but benefits are fixed—not unlimited

What Is Hospital Indemnity Insurance and Do You Need It?

At its core, hospital indemnity insurance is a type of supplemental insurance that pays you cash benefits directly when you’re hospitalized due to illness or injury.

How It Works (Simple Breakdown)

- You pay a monthly premium (often $10–$60)

- If hospitalized, the policy pays:

- A lump sum (e.g., $1,000 admission benefit)

- A daily benefit (e.g., $100–$300 per day)

- The money goes directly to you, not the hospital

You can use the payout for anything:

- Deductibles and copays

- Rent or mortgage

- Groceries or childcare

- Lost income

👉 Key Point: This is not a replacement for health insurance—it’s a financial cushion.

Why This Insurance Exists (And Why It’s Growing Fast)

Healthcare costs in the U.S. remain unpredictable. Even with employer-sponsored coverage, many Americans now have high-deductible health plans (HDHPs).

- Average hospital stay cost: $10,000–$30,000+

- Typical deductibles: $1,500–$5,000+

- Out-of-pocket max can exceed $8,000

If you can’t comfortably absorb those costs, hospital indemnity insurance fills that gap.

Key Features and Benefits

1. Direct Cash Payments

Unlike traditional insurance, payouts go straight to your bank account.

2. Flexible Spending

Use the money however you want—medical or non-medical.

3. Predictable Benefits

You know exactly what you’ll receive (fixed amounts).

4. Easy Enrollment

Many employer plans require:

- No medical exam

- Minimal underwriting

5. Coverage Extensions

Some plans also include:

- ICU stays

- Ambulance services

- Outpatient surgery

Hospital Indemnity Insurance Pros and Cons

Pros

- Financial safety net during emergencies

- Helps cover high deductibles

- Affordable premiums

- Works alongside existing insurance

- Useful for planned events (like childbirth)

Cons

- Limited coverage (fixed payouts, not full bills)

- Doesn’t replace health insurance

- May not be needed if you have strong savings

- Some policies have waiting periods or exclusions

Is Hospital Indemnity Insurance Worth It?

The answer depends on your financial situation—not just your health.

It’s Usually Worth It If:

- You have a high-deductible health plan

- You don’t have a large emergency fund (3–6 months)

- You’re planning a hospital event (like pregnancy or surgery)

- You’re self-employed or have unstable income

It May NOT Be Worth It If:

- You already have strong savings

- Your employer covers most hospital costs

- You rarely face hospitalization risks

👉 Real-World Insight:

Commonly, individuals underestimate indirect costs—missed work, childcare, transportation—which this policy helps cover.

Hospital Indemnity Insurance for Seniors

For older adults, hospitalization risk increases significantly.

Why Seniors Consider It:

- Medicare still has gaps (deductibles, coinsurance)

- Fixed incomes make unexpected bills harder to absorb

- Hospital stays are more frequent and longer

Best Use Case:

Pairing it with Medicare Advantage or Medigap plans to reduce financial strain.

Hospital Indemnity Insurance for Pregnancy: Is It Worth It?

This is one of the most searched—and practical—use cases.

Average Cost of Childbirth in the U.S.:

- Vaginal delivery: $10,000–$15,000

- C-section: $15,000–$25,000+

Even with insurance, out-of-pocket costs can reach $3,000–$6,000.

Why It Works for Pregnancy:

- You know hospitalization will happen

- Policies often pay:

- Admission benefit

- Daily stay benefit

- Sometimes newborn care

Important Catch:

- Most plans have a waiting period (9–12 months) for pregnancy

- You must enroll before becoming pregnant

👉 Answer:

Yes, hospital indemnity insurance is often worth it if pregnant—but only if you enroll early.

Hospital Indemnity Insurance for Individuals (Self-Employed & Freelancers)

If you’re self-employed, your financial risk is higher.

Why It Matters:

- No employer-paid benefits

- Income stops if you’re hospitalized

- High-deductible marketplace plans are common

This insurance acts like:

- Income protection (short-term)

- Emergency fund backup

What Does Hospital Indemnity Insurance Typically Cover?

Most plans include:

- Hospital admission (lump sum)

- Daily hospital stay

- ICU stays (higher daily rate)

- Surgery (sometimes)

- Emergency room visits

Some advanced plans also include:

- Mental health hospitalization

- Rehabilitation stays

How Much Does Hospital Indemnity Insurance Cost?

Average Monthly Premiums (2026 Estimates)

- Individual: $15–$40/month

- Family: $40–$100/month

What Affects Pricing:

- Age

- Coverage level

- Benefit amounts

- Employer vs individual plan

👉 Compared to traditional insurance, this is low-cost protection.

How to Get a Hospital Indemnity Insurance Quote

You can get a hospital indemnity insurance quote through:

- Employer benefits portal

- Insurance companies (Aflac, MetLife, Guardian, etc.)

- Online comparison tools

What to Compare:

- Daily benefit amount

- Admission payout

- Waiting periods

- Coverage limits

- Exclusions

What People Are Saying (Hospital Indemnity Insurance Reddit Insights)

Across forums like Reddit, users share mixed—but insightful—experiences:

Positive Feedback:

- “Paid for my deductible after a surgery”

- “Worth it for childbirth alone”

- “Cheap peace of mind”

Criticism:

- “Didn’t use it for years”

- “Coverage felt limited”

👉 Takeaway:

It’s most valuable when you actually use it—which makes timing and life stage critical.

Pro Tip: When This Insurance Delivers Maximum Value

💡 Pro Tip:

Hospital indemnity insurance delivers the highest ROI when you can predict hospitalization—like pregnancy, planned surgeries, or managing chronic conditions.

Tax Considerations (U.S. Context)

- Premiums are typically paid after-tax

- Benefits received are usually tax-free (under current IRS rules)

For complex situations, consult a licensed advisor or review guidance from the Internal Revenue Service.

Actionable Next Steps

If you’re considering hospital indemnity insurance, here’s exactly what to do next:

1. Evaluate Your Risk

- Do you have upcoming medical events?

- Can you cover a $5,000 bill tomorrow?

2. Check Your Current Insurance

- Review deductibles and out-of-pocket max

3. Compare 2–3 Quotes

- Focus on benefit amounts—not just premiums

4. Time It Right

- Especially critical for pregnancy coverage

5. Don’t Overbuy

- Match coverage to realistic needs—not fear

Financial Disclaimer

This article is for informational purposes only and does not constitute financial, insurance, or tax advice. Coverage options, pricing, and tax treatment may vary based on individual circumstances and state regulations. Always consult with a licensed insurance professional or financial advisor before making decisions.

{kind=link}